Getting Tired of burial policies for seniors? 10 Sources of Inspiration That'll Rekindle Your Love

The 5-Second Trick For Health Insurance Glossary - Health Insurance Definitions And ...

In Britain more extensive legislation was presented by the Liberal government in the 1911 National Insurance Coverage Act. This gave the British working classes the very first contributory system of insurance coverage versus illness and joblessness. This system was greatly expanded after the Second World War under the influence of the Beveridge Report, to form the very first modern well-being state.

The insured entities are for that reason safeguarded from threat for a fee, with the fee depending on the frequency and intensity of the occasion taking place. In order to be an insurable risk, the risk guaranteed against need to fulfill particular qualities. Insurance coverage as a monetary intermediary is a commercial enterprise and a huge part of the monetary services market, but specific entities can also self-insure through conserving cash for possible future losses.

Exceptions consist of Lloyd's of London, which is famous for ensuring the life or health of actors, sports figures, and other famous people. Nevertheless, all exposures will have specific distinctions, which might cause various premium rates. Certain loss: The loss occurs at a recognized time, in a recognized place, and from a known cause.

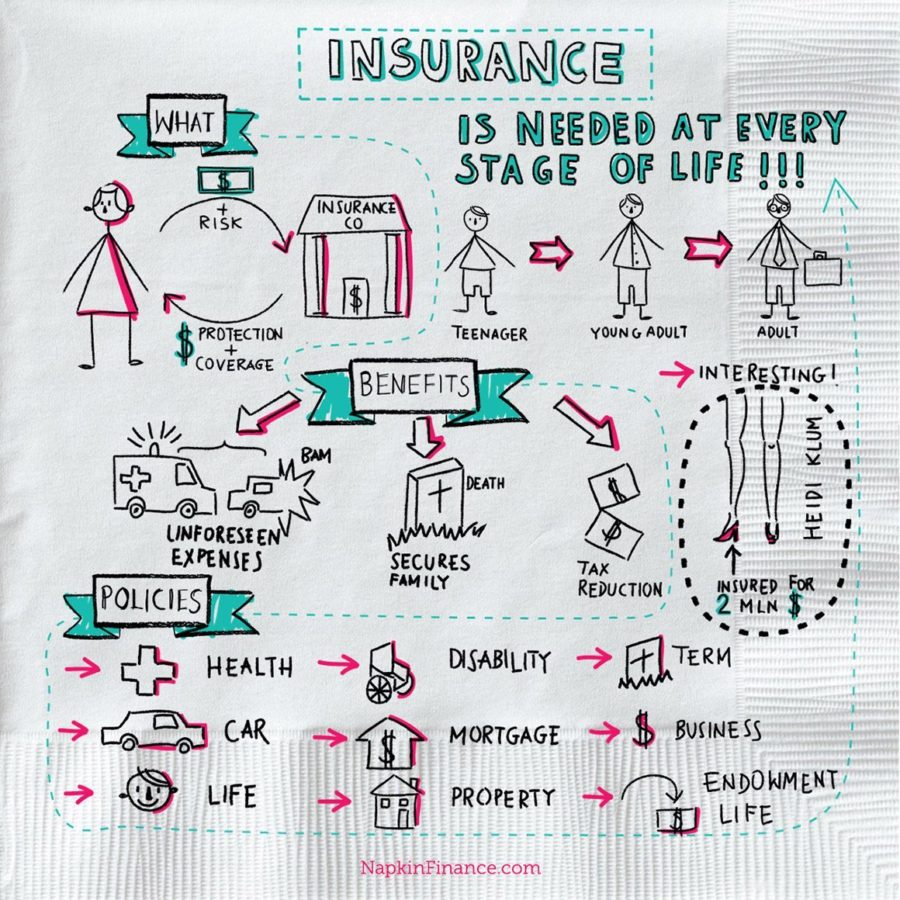

Our Insurance : Importance, Types And Benefits - Cleartax PDFs

Fire, car accidents, and worker injuries may all quickly fulfill this requirement. Other kinds of losses may only be certain in theory. Occupational disease, for example, might involve extended direct exposure to injurious conditions where no particular time, location, or cause is identifiable. Preferably, the time, location, and cause of a loss ought to be clear enough that a reasonable individual, with adequate information, might objectively validate all 3 elements.

The loss needs to be pure, Great site in the sense that it arises from an occasion for which there is just the opportunity for cost. Occasions which contain speculative components such as common business risks or even purchasing a lottery ticket are normally not thought about insurable. Large loss: The size of the loss must be meaningful from the perspective of the guaranteed.

For small losses, these latter costs might be several times the size of the expected expense of losses. There is hardly any point in paying such expenses unless the security used has genuine worth to a purchaser. Affordable premium: If the possibility of an insured event is so high, or the cost of the event so large, that the resulting premium is big relative to the amount of protection provided, then it is not most likely that the insurance will be bought, even if on deal.

What Does What Is Insurance? - Facts On Insurance Do?

/insurance-faa9df3f80274172970efdd638aca3cb.jpg)

If there is no such chance of loss, then the deal might have the type of insurance, but not the substance (see the U.S. Financial Accounting Standards Board pronouncement number 113: "Accounting and Reporting for Reinsurance of Short-Duration and Long-Duration Contracts"). Calculable loss: There are 2 aspects that should be at least estimable, if not officially calculable: the likelihood of loss, and the attendant expense.

Restricted risk of catastrophically big losses: Insurable losses are ideally independent and non-catastrophic, indicating that the losses do not take place all at once and specific losses are not extreme sufficient to bankrupt the insurer; insurers might prefer to restrict their direct exposure to a loss from a single occasion to some little portion of their capital base.

In the United States, flood threat is insured by the federal government. In industrial fire insurance coverage, it is possible to find single homes whose overall exposed worth is well in excess of any private insurer's capital constraint. Such residential or commercial properties are generally shared amongst numerous insurance companies or are guaranteed by a single insurance provider who syndicates the danger into the reinsurance market.

Fascination About 'Insured To Value' Definition - Union Mutual Insurance

A number of commonly cited legal concepts of insurance coverage consist of: Indemnity the insurance company indemnifies or compensates, the insured when it comes to specific losses only approximately the insured's interest. Advantage insurance coverage as it is specified in the research study books of The Chartered Insurance Institute, the insurer does not have the right of recovery from the celebration who caused the injury and is to compensate the Guaranteed despite the reality that Insured had currently sued the negligent celebration for the damages (for example, personal mishap insurance) Insurable interest the insured normally must directly experience the loss.

The concept needs that the guaranteed have a "stake" in the loss or damage to the life or home guaranteed. What that "stake" is will be identified by the kind of insurance included and the nature of the residential or commercial property ownership or relationship in between the persons. The requirement of an insurable interest is what differentiates insurance from gambling.

Material facts must be divulged. Contribution insurance companies which have similar obligations to the insured contribute in the indemnification, according to some method. Subrogation the insurance provider gets legal rights to pursue healings on behalf of the guaranteed; for instance, the insurer might sue those responsible for the insured's loss. The Insurance companies can waive their subrogation rights by using the unique stipulations.

Miley Cyrus and burial policies for seniors: 10 Surprising Things They Have in Common

What Are The Different Types Of Insurance - General & Life ... for Beginners

/GettyImages-1053743626-3b1327252ce94a998c9508c06fed8eea.jpg)

If the Insured has a "compensation" policy, the insured can be needed to spend for a loss and after that be "compensated" by the insurance coverage provider for the loss and out of pocket expenses including, with the authorization of the insurer, claim expenditures. Under a "pay on behalf" policy, the insurance provider would defend and pay a claim on behalf of the guaranteed who would not run out pocket for anything.

Under an "indemnification" policy, the insurance provider can generally either "repay" or "pay on behalf of", whichever is more useful to it and the insured in the claim dealing with procedure. An entity seeking to move danger (a person, corporation, or association of any type, etc.) ends up being the 'insured' party once risk is presumed by an 'insurance provider', the guaranteeing celebration, by methods of a agreement, called an insurance plan.

An insured is thus stated to be "indemnified" versus the loss covered in the policy. When guaranteed parties experience a loss for a specified peril, the protection entitles the insurance policy holder to make a claim versus the insurance provider for the covered amount of loss as defined by the policy. The fee paid Great site by the insured to the insurer for presuming the risk is called the premium.

Getting My What Is Auto Insurance? - Iii To Work

So long as an insurance company keeps appropriate funds set aside for expected losses (called reserves), the staying margin is an insurance provider's revenue. Policies normally consist of a number of exemptions, consisting of normally: Insurance coverage can have various results on society through the manner in which it alters who bears the expense of losses and damage.

Insurance coverage can affect the probability of losses through moral danger, insurance fraud, and preventive steps by the insurer. Insurance coverage scholars have normally utilized moral hazard to refer to the increased loss due to unintentional recklessness and insurance fraud to describe increased threat due to deliberate carelessness or indifference.

While in theory insurance providers could encourage financial investment in loss reduction, some commentators have actually argued that in practice insurance companies had historically not aggressively pursued loss control measuresparticularly to avoid disaster losses such as hurricanesbecause of concerns over rate reductions and legal battles. However, given that about 1996 insurance companies have actually started to take a more active role in loss mitigation, such as through building codes.

The Best Guide To Insurance Explained - Cib

However, in case of contingency insurance coverages such as life insurance, double payment is enabled) Self-insurance situations where threat is not transferred to insurance provider and entirely kept by the entities or individuals themselves Reinsurance situations when the insurance company passes some part of or all threats to another Insurer, called the reinsurer Accidents will occur (William H.

Collection EYE Movie Institute Netherlands. Insurance companies may utilize the subscription business design, gathering premium payments periodically in return for on-going and/or intensifying benefits provided to policyholders. Insurers' organization design aims to gather more in premium and investment earnings than is paid out in losses, and to also use a competitive rate which consumers will accept.

Insurers earn money in 2 ways: Through underwriting, the process by which insurers select the risks to insure and decide how much in premiums to charge for accepting those dangers, and taking the brunt of the danger ought to it concern fulfillment. By investing the premiums they gather from insured parties The most complex element of guaranteeing is the actuarial science of ratemaking (price-setting) of policies, which uses statistics and probability to approximate the rate of future claims based on a provided danger.

The Main Principles Of What Is Auto Insurance? - Iii

At one of the most fundamental level, preliminary rate-making involves taking a look at the frequency and seriousness of insured dangers and the expected average payout resulting from these dangers. Thereafter an insurance coverage company will gather historic loss-data, bring the loss data to present worth, and compare these prior losses to the premium gathered in order to assess rate adequacy.

Rating for different risk qualities includes - at the a lot of basic level - comparing the losses with "loss relativities" a policy with two times as many losses would, for that reason, be charged two times as much. More intricate multivariate analyses are often utilized when multiple qualities are involved and a univariate analysis could produce puzzled results.

Upon termination of a given policy, the amount of premium collected minus the quantity paid out in claims is the insurer's underwriting earnings on that policy. Financing efficiency is determined by something called the "combined ratio", which is the ratio of expenses/losses to premiums. A combined ratio of less than 100% suggests an underwriting profit, while anything over 100 suggests an underwriting loss.